How could they fall for that?!

How could they fall for that?!

The promise of technology can be made investor fool's gold, either deliberately or because of a winner's curse.

The inspiration for this post was Patrick Boyle's video below:

TL;DW: An inventor, John Keely, kept promising miraculous products without ever delivering, for 26 years; his demonstrations were, not to put too fine a point on it, fraud. Watch the video for the hilarious details.

Yesterday’s miracle is tomorrow’s commodity

What's this fixation on new new new things about?

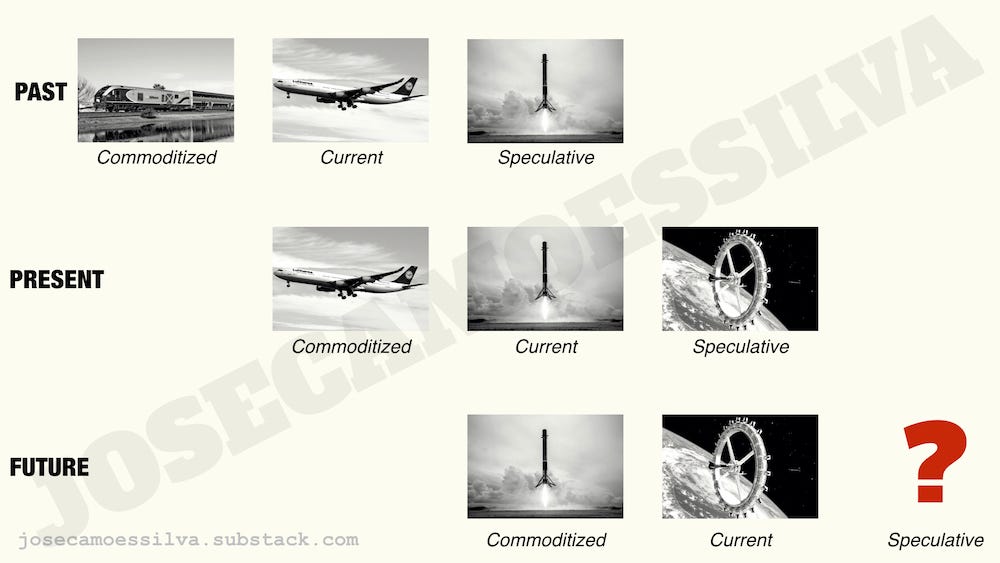

For any new product or innovation brought to mass market there’s a generic life cycle that begins with it being an experience: having the "wow" factor of novelty, the ability to do new things or old things in a better way, and the identity marker of having something others don't have.

Then it becomes a product: something that has a core function but also delivers additional value; a Ferrari Monza SP2 and a SMART ForTwo have the same function, moving two people on roadways, but different target markets and capabilities.

And eventually it becomes a commodity, nothing more than a core function, for all practical purposes; sometimes with the “help” of the companies selling it: airline codesharing certainly makes the point that passengers should only care about the core function of air travel and price.1

(There’s a popular marketing book that presents this evolution in the wrong direction, because the authors looked at a snapshot of the market and assumed it was a time series. That’s literally the nicest thing that can be said about that book.)

Experiences are more profitable than products and products more profitable than commodities, generally speaking. So, to address the inexorable commoditization of their offerings, companies need to innovate, innovate, innovate. Figuring out which innovations will become experiences rather than write-offs is a nontrivial problem.

At a more macro level, technologies (ways to solve a problem with stuff rather than labor) follow a similar pattern across longer time scales. For example:

The red question mark is the big deal here: because we’re looking very far from our current experience, there’s a broad distribution of possibilities; the way we deal with the uncertainty in that distribution creates a well-known problem, that of the winner’s curse.

Winner's curse in technology investing

(For more detail on the winner's curse, see Jose Silva's intergalactic best-selling2 book DATA to INFORMATION to DECISION and ten things people get wrong about numbers, data, and models; free sample here.)

There's a well-known phenomenon in resource auctions called the winner's curse, where the winner of the auction may end up losing money.

The mechanism is simple: the resource has a value that is common to all the bidders (there's some fixed amount of oil in a prospect) and each bidder gets some data about that value, on which they base their bids; the winning bid is from the bidder with the highest estimate of the value; but since the estimate includes the common value (equal for all bidders) and estimation error, the winner is the one with the highest value for the error, the one that over-estimates the value the most. Hence, the highest bidder, and winner, may lose money.

We can apply this logic to long-shot technology investments, for example establishing a Mars colony.

Let's say that the variable of interest for investment is how long until there’s a self-sufficient colony in Mars. There are several visionaries proposing different approaches, and each approach has its distinct characteristics. But most of the difficulties establishing a Mars colony have to do with the current state of technology and the problems of having humans on Mars (including some unknown unknowns); that's the common value in the process.

So, there’s a part of the visionaries’ plans that suffers from winner’s curse: the more optimistic visionaries will be the ones with the shortest estimate of the time to self-sufficiency on Mars; part of that will be overestimation of their own capabilities, but some will be an overestimation of the speed of evolution of the technology and science needed, a common value (and thus a precursor of the winner’s curse).

As a result, some of these visionaries may come across as confidence artists, trying to get paid for something that others believe is far more difficult than the visionaries’ proposals; and because of the winner’s curse, the results may even support that assessment.

But it might be just a matter of choices based on extremes (investing in the more optimistic of the long-shot projects) when they should be based on means (maintaining a portfolio of different approaches, some optimistic, some pessimistic, some neutral).

The more visionaries, the worse the problem

As the number of visionaries increases, the problem becomes worse: as the winner’s curse is a function of the maximum (or the higher order statistics, for any pedantic readers), the more visionaries, the higher the expected deviation from the mean.

The following figure illustrates the increasing winner's curse with number of visionaries. It shows the distribution of the maximum of 1000 (blue) or 2000 (red) draws from a standard Normal distribution3 (meaning that the mean value, the correct value to bid in a resource auction, would be zero):

Note how the red (2000 visionaries) distribution is to the right (higher values) of the blue (1000 visionaries) distribution: not only are the most speculative ideas in the group with 2000 typically more speculative than those in the group with 1000, but many of the highly-speculative ideas in the group with 1000 are close to the middle of the distribution for the group with 2000.4

In other words, when the number of visionaries increases, not only do the extreme ideas become more extreme, but what used to be extreme ideas in a smaller group now appear to be modestly speculative. There’s no strategic element to the rationale above, but it’s not hard to see that introducing competition for financing makes this worse: the more visionaries there are, the more difficult it’ll be for a modestly speculative idea to not appear too timid.

To be fair, there's also a good chance that these long-shot projects, given their lack of ongoing success metrics and expected high incidence of failures, may attract some confidence artists. But not all failures are evidence of confidence artistry.

(Note that if we were looking at means, increasing the number of visionaries would give us a better estimate of the mean; but as we’re looking at extremes, we get more error with more visionaries. There's an entire chapter about the pitfalls of extremes versus means in the aforementioned intergalactic best seller, free sample here.)

Still, how could anyone fall for that?!

A new form of energy. Promises of ever new products that never come to fruition. Refusal to do even the simplest demonstrations proposed by journalists. Surely these were red flags. Keely got a way with it for 26 years. Twenty-six. That’s… something.

Perhaps we could ask the investors in Theranos, a company that had more red flags than a communist May Day parade.

There's a basic FOMO5 in operation in the Theranos case: some people thought that microfluidics (using microchip-like technology to replace larger biochemistry lab equipment; Theranos had claimed to have operational microfluidics hardware6) were "the next big thing," and they didn't want to be known as the money manager who passed on investing in the next Intel, Xerox, Apple, Microsoft, Google, or Facebook.

And the CEO wore a black turtleneck!

To be fair, airlines never miss an opportunity to make a great case for general aviation (flying private). That’s what happens when you put accountants in charge of strategy, marketing, and operations.

We're booking mostly sales from M31 Andromeda; we can trust the numbers, Arthur Andersen has audited them.

In the spirit of showing one's work, readers can replicate the results for any number of draws NDraws by using the following snippet of R code:

NDraws <- 2000sim <- c(1:100000)for(i in 1:100000){ sim[i] <- max(rnorm(NDraws)) }hist(sim)To preempt any confusion, this is not one of those “fat tails” problems some people make a career grumbling about (while blocking anyone who points out that not all fat-tailed distributions are extreme-dominated distributions). Sadly this preemption is justified by previous interactions with fans of the biggest grumbler.

“Fear of missing out,” as the kids say; not “Fed open market operations.”

Many lab equipment, pharmaceutical, and chemical companies have campuses filled with researchers that had been working in microfluidics for years (some, decades) when Theranos announced it had solved the problem.

The main problem with microfluidics is that fluids aren't electrons and confining them in small spaces makes them behave in complicated and counter-productive ways. There's also the destructive nature of many of the clinical tests done on those fluids and the problem that the fluids themselves are not homogeneous at small scales, so a micro-sample might not contain a representative sample of chemicals and biologicals.

To believe that a chemical engineering drop-out could have solved the problem that vexed a large population of scientists for years/decades using some Silicon Valley magic beans was as much a sign of willful ignorance as anything that Keely did.

Not just a problem on the cutting edge. My day job has various troubles because it went into production before testing was complete. Now we have to retrofit fixes to hundreds of airplanes. Obviously a bad idea, but the Pentagon wanted a new fighter and Congress wanted assurances it would be cheap. So the politicians were told the lies they wanted to hear.